How to give yourself an interest rate cut and save thousands on your home or investment loan even if the reserve bank doesn’t on Tuesday?

If you’re in property you probably realise we are in an environment of historic low interest rates with the chance they could even go lower.

There are probably people reading this saying ‘yeah I wish I could get a piece of those’. Because that is the reality, even though interest rates are low many investors can’t get them according to leading Australian consumer and financial law firm MyCRA Lawyers.

Why is that? Well that’s because the banks and other lenders are using comprehensive credit reporting or CCR as an excuse to raise interest rates on a case by case basis and chances are you won’t know you’ve been impacted until you go for your next loan according MyCRA Lawyers CEO Graham Doessel.

What is Comprehensive Credit Reporting and how it catches out unsuspecting property buyers?

“It used to be the case that your credit file only recorded when you were really naughty. Like not paying your creditors or if you shopped around a lot for credit. Well about 18 months ago credit reporting changed and comprehensive credit reporting was introduced,” Mr Doessel said.

“Why did this happen, well the idea was it would give lenders a more realistic picture of what a potential borrower looked like.

“What it means for the borrower is now whether you like it or not many bills you pay on a regular basis are being recorded on your credit file,” Mr Doessel said.

“So your home loan, credit card, car loans, store cards and the like are being tracked in relation to your repayment history. And while they aren’t just yet pretty soon power bills and phone bills will be tracked as well,” Mr Doessel said.

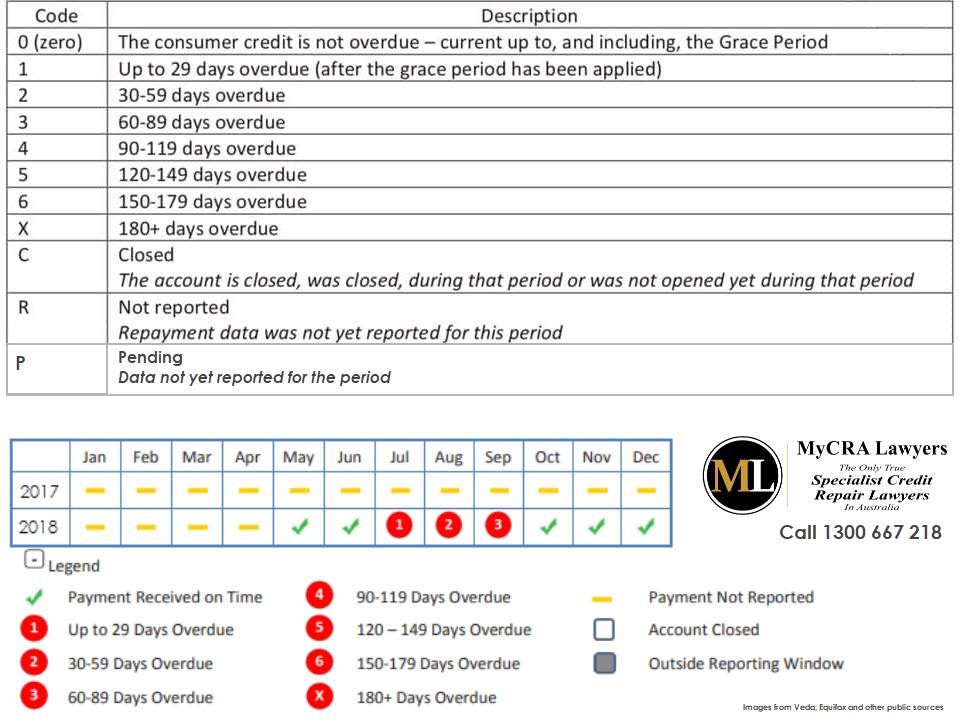

“Every time you pay one of these late by 14 days or more it’s recorded. So if you’re 14 to 30 days late you will get a 1, 5 months late you get a 5 anything over 6 months and you get an X.

MyCRA Lawyers – Equifax Repayment History Information (RHI) Legend – Call Now 1300 667 218

“Just a 1 on your file will be enough for a bank offering the best rates to ratchet up their interest or reject you and force you to go see a second tier lender and trust me you don’t want to go there.

“Before I went back to university and then opened my own law firm I used to deal with these lenders when I was trying save people from foreclosure and they want their pound of flesh and if they don’t get it they will dismember you asset by asset, Mr Doessel said.

How comprehensive credit reporting allows the banks to put you over a barrel.

“Whether buying for investment or as an owner occupier not too many people would purchase without first having a chat with the bank before raising their hand at auction or making a formal offer.

“It’s when you return to the bank to sign on the dotted line and the bank knows you are committed to buy and committed to borrowing with them the bank pulls out your comprehensive credit report.

“If your file it’s clean you are fine and they aren’t going to have any reason to ratchet up your rate. But if you have recently made an enquiry with a one of these new buy now pay later services, or looked at credit cards chances are it will be on your file and the bank will use this to raise your interest rate,” Mr Doessel said.

Why? Because if you can’t afford to buy something for a couple of hundred bucks up front, well, you maybe a credit risk according to the bank, Mr Doessel said.

“Or perhaps you changed address and missed a couple of bills, after all you weren’t silly enough to buy before you’d sold your house, but you did forget to change the address to your mother-in-laws for the three months you lived down stairs while you found the dream home you just signed on the bottom line for. Those late payments are all on your credit file and will impact your loan application and interest rate,” Mr Doessel said .

“Comprehensive credit reporting is much like a driver’s licence, you start out with a full set of points, 1200 to be exact and every time you do something wrong you lose some.

“It doesn’t even have to be wrong necessarily, it’s more something financially careless according to those who make the lending rules.

“If you get to the point where you have less than 500 points then you will lose your licence to borrow. Everything in between will be just like trying to get car insurance with a bad driving record, yes, you can get it, but you will pay more,” Mr Doessel said.

What else might surprise people, is often mistakes are made on credit files, not by you but by the financial institutions filing reports. They could report someone else’s bad deeds on your file because the name is similar or make an unauthorised enquiry into your credit, that is some over zealous loan broker wants to check your credit worthiness without telling you and it comes up on your file.

“Commonly we have clients with defaults listed on their file where the credit agency didn’t go through the proper process. How common is this? Well more than 3.8 million Australians have these on their credit file and don’t know. How do you know? Well check your credit file at www.freecreditrating.com.au for a start,” Mr Doessel said.

How can I give myself an interest rate cut?

So the bank won’t give you the sweet deal they have in big writing in the branch window, because they reckon your credit file is dirty.

All because Comprehensive Credit Reporting now tracks your repayment history and 14 days late is enough to see you put on the naughty list and banks aren’t as forgiving as Santa.

“But I was pre-approved” I hear you say with tears in your eyes as you calculate your new monthly repayments at the higher interest rate and the dream of home ownership with occasional overseas holiday starts to look more like suburban servitude with the bank your all seeing master that will control your wallet for the next 3 decades.

So what can you do to clean it up?

“The easiest way is not to blot your copy book to start with. How, well, pay your bills on time, don’t default on loans and most importantly don’t shop around for credit by entering your details and seeing if you are approved,” Mr Doessel said.

“You can get a list of the best lenders from a host of websites whether it’s home loans, credit cards, personal loans or buy now pay later services, you don’t need to give them your details until you are ready to move forward with a purchase,” Mr Doessel said.

You can check your credit file free and easily and you can do it once a year at www.freecreditrating.com.au.

If your credit rating is bad or less than perfect and you have got some enquiries on your file the bank may use this to up your interest.

The good news is, in most cases these can be removed, because for a credit provider to mark your credit file they need your permission, which you probably gave them as you clicked through the terms and conditions agreement on their website (nobody reads that and they know it), but that still doesn’t mean they have to stay there.

“Here at MyCRA Lawyers we have honed the processor removing these files and in most cases can have these removed within 7 days from your file. Straight away you should then be able to access a lower interest rate,” Mr Doessel said.

“The next blot are defaults and default judgements, these are a little more serious, but we can get them removed. It is a legal process that can only be performed by a registered solicitor but one we have pioneered over the past decade.

“As you see these defaults and enquiries removed you will see a direct correlation as your credit score goes up the interest rates you can access go down.

“The savings can be huge, depending on the size of your loan, we are talking tens of thousands of dollars a year and over the life of a loan the savings can go into the hundreds of thousands of dollars,” Mr Doessel said.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment